Agent Banking 101 : A Guide for Product Managers

According to the World Bank’s Global Findex Database (2021), around 1.4 billion adults globally are unbanked and Sub-Saharan Africa carries a heavy share of that number. In Nigeria, about 32% of adults are either unbanked or underbanked meaning they lack access to consistent, reliable financial services but operate in cash economies outside the formal system.

This exclusion isn’t just about not having a bank account. It means people can’t save securely, can’t build a credit history, can’t easily pay for utilities, and often get locked out of opportunities to grow their businesses or improve their livelihoods.

This is the gap agency banking is designed to fill. Instead of financial institutions investing millions in new branches that take years to break even, they leverage existing micro-entrepreneurs. The local kiosk, the neighbourhood grocer or the market woman becomes a financial service touchpoint. With a POS device, mobile phone or platform an agent can handle deposits, withdrawals, bill payments, transfers open accounts and more.

For customers, this means financial access within walking distance, often from someone they already know and trust. For banks and fintechs, it means rapidly extending distribution into areas that were previously unreachable at a fraction of the cost.

In this article, I’ll walk you through agency banking through the lens of a product manager working in the Nigerian market. We’ll cover why it matters, the models that exist, who qualifies to be an agent, and the categories recognised by regulations. I’ll also highlight what agents are allowed (and not allowed) to do, how revenue flows through the system, and the critical considerations financial institutions must weigh before deciding to launch or scale an agency network.

By the end, you’ll have a clear picture of how agency banking works in Nigeria, the rules that shape it, and the product decisions that determine whether it succeeds or fails.

Before we go further, let’s answer the obvious question: what exactly is agency banking? Is it just a shop with a POS? or something more structured ?

Let’s start with the definition.

According to the Guidelines for the Regulation of Agent Banking and Agent Banking Relationships in Nigeria, Agent banking is the provision of financial services to customers by a third party (agent) on behalf of a licensed deposit-taking financial institution and/or mobile money operator (principal).

Agency banking is, therefore, a model where banks and licensed financial institutions deliver services through these third-party agents instead of only relying on their own branches or ATMs. These agents are usually existing small businesses, such as shopkeepers, market traders etc, who are equipped with the tools and authorisation to perform basic financial transactions on behalf of a bank.

In practical terms, an agent becomes a “human ATM” or “mini-branch” in their community. With a POS terminal, mobile app, or dedicated platform, they can help customers deposit money, withdraw cash, pay bills, transfer funds, open new accounts and much more.

In Nigeria, Regulators, such as the Central Bank of Nigeria (CBN), in Nigeria have issued guidelines and regulations to formalise and monitor the practice, ensuring that agents operate safely while working to improve financial inclusion.

So, at its core:

The bank provides the license, technology, and settlement infrastructure.

The agent provides the human face and access point.

The customer gains convenient entry into formal financial services.

Why Agency Banking Matters

1. Expands Distribution Channels

Think of agency banking as building a network of mini-branches without the cost of real estate. Every time a bank signs up a shopkeeper, pharmacy, or local kiosk as an agent, it creates a new access point for customers. This is a ready-made distribution network that can dramatically extend the reach of your product into areas that would otherwise be hard to penetrate.

In rural towns, agents often become the bank for entire communities.

In urban centres, they provide quick access for customers who don’t want to queue at branches.

2. It Reduces Acquisition Costs

Acquiring new customers through branches is expensive. Acquiring them purely online often assumes smartphone literacy, trust, and data access that some people don’t yet have. Agency banking lowers the barrier.

When a customer walks into their neighbourhood shop and performs their first transaction through a trusted agent, they’re more likely to adopt other services. The acquisition happens at low cost because:

The agent already has community trust (reducing the need for heavy brand marketing).

Infrastructure costs are shared (the shop is already there).

Customers onboard faster when the process is simple, human, and local.

3. Drives Financial Inclusion as a Business Growth Strategy

Financial inclusion is often framed as a social good, and it is. But for financial institutions, it’s also an effective business strategy. In Nigeria, where millions of adults are still unbanked or underbanked, every person who gains access to formal financial services represents both a social impact and a new revenue opportunity.

Agency banking plays a central role in this. It gives customers their first step into the financial system, usually through basic transactions like deposits or withdrawals, at a local agent they already trust. This “first step” matters because it lowers the psychological and logistical barriers that keep many people out of the banking system.

But the real business value emerges after that first step. Once customers are onboarded, institutions can cross-sell higher-value products such as

Savings accounts

Microloans

Insurance products

Bill payments and transfers

Every newly included customer is a potential long-term user whose lifetime value grows as they move up the financial services ladder.

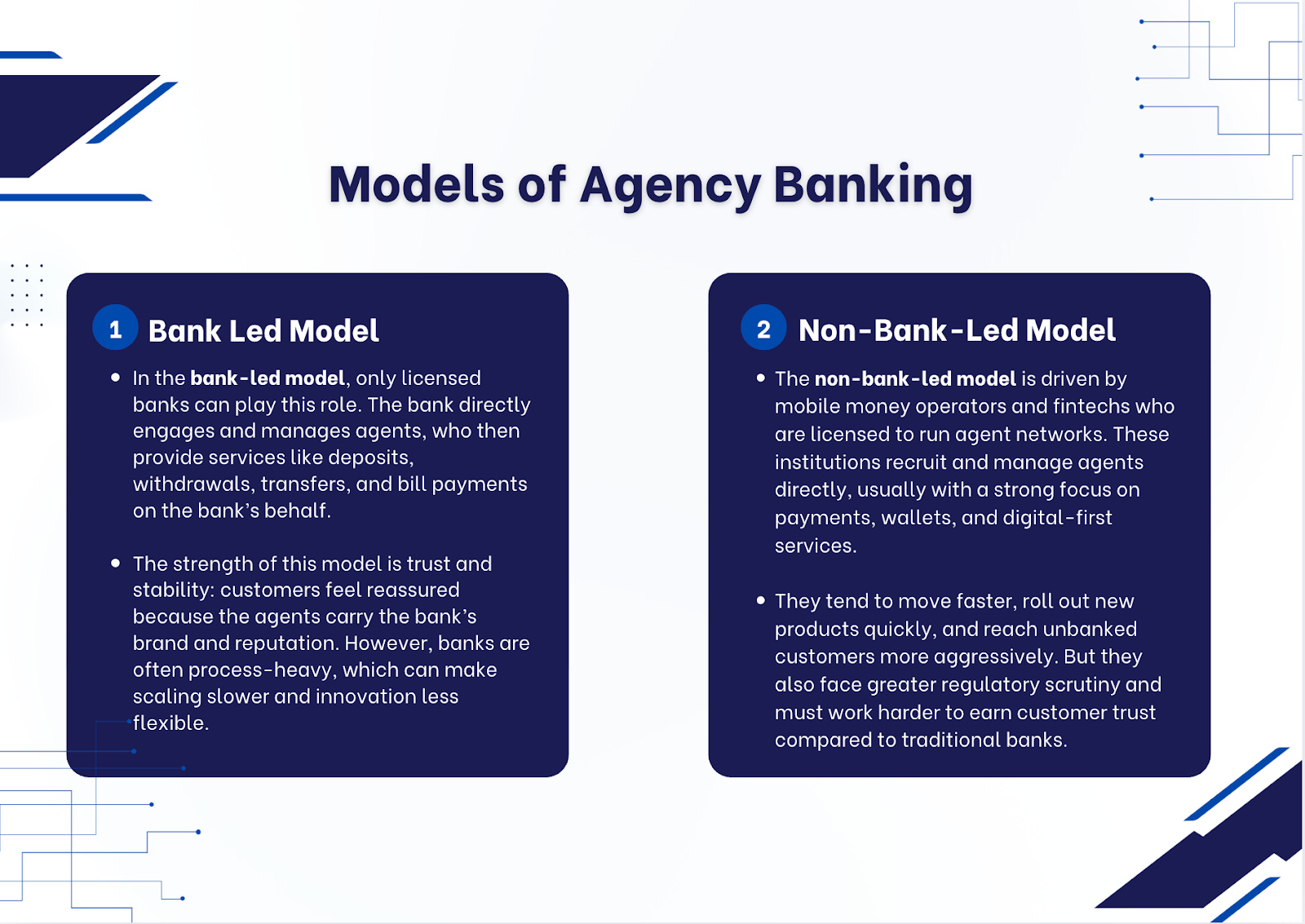

Models of Agency Banking

There are two main ways agency banking can be structured: the bank-led model and the non-bank-led model. The difference lies in who acts as the principal, i.e the institution that contracts and supervises the agents.

Who Can Become an Agent?

Not every business is eligible to serve as a banking agent. The Central Bank of Nigeria (CBN) sets clear criteria to ensure that agents are credible, established, and capable of handling financial transactions responsibly.

Eligible Entities:

To qualify, a business must have been in legitimate commercial activity for at least 12 months before applying. The types of entities that can become agents include:

Limited liability companies

Sole proprietorships

Partnerships

Cooperative societies

Public entities

Trusts

Any other entity the CBN may approve

In practice, this means that a neighbourhood shop, a fuel station, or even a cooperative society can be authorised as an agent, provided they meet the requirements.

Entities That Cannot Become Agents: The guidelines specifically exclude some organisations. These include:

Faith-based organisations (churches, mosques, etc.)

Non-governmental organisations (NGOs)

Educational institutions

Bureau de change operators

Any entity prohibited by law from carrying out profit-making business.

Additional Requirements:

The business must be a going concern (not dormant or insolvent).

It must not have a history of fraud, dishonesty, or unresolved credit defaults.

The entity must have the infrastructure and staff to handle cash and electronic transactions.

If the business is already regulated by another authority, it must first obtain approval from that authority before becoming an agent,

Types of Agents

Agents are classified into three main categories, each with a different role in the value chain.

1. Super Agents

Super Agents are licensed entities that manage and onboard individual agents under their network. Super agents are the “big players.” They are directly contracted by a bank or mobile money operator and are allowed to build a network of sub-agents under them. Think of them as wholesalers in the system. They don’t just serve customers themselves, but also recruit, train, and manage other agents. Super agents are also responsible for ensuring liquidity support for their sub-agents, making them a critical backbone of scale.

2. Sole Agents

A sole agent is engaged directly by a financial institution and operates independently. They don’t have sub-agents under them and are solely responsible for their own outlet. These are typically small businesses like a neighbourhood shop or pharmacy that directly serve customers in their community.

3. Sub-Agents

Sub-agents work under the umbrella of a super agent. They are the “last-mile” touch points, usually small shop owners or traders equipped with a POS device or mobile app. While they interact directly with customers, they rely on the super agent for liquidity, training, and oversight.

Permissible Activities for Agents

Agents are allowed to carry out the following services:

Cash deposit and withdrawal

Bill payments (utilities, taxes, subscriptions, etc.)

Payment of salaries

Local funds transfer services

Balance enquiries and mini statements

Collection and submission of account opening/KYC documents

Agent-enabled mobile banking services

Loan disbursement and repayment collection

Cash payment of retirement benefits

Cheque book requests and collection

Collection of bank correspondence for customers

Other activities the CBN may prescribe from time to time

Prohibited Activities for Agents

Agents are expressly barred from:

Operating when there’s communication failure with the bank

Carrying out transactions where a receipt/acknowledgment cannot be generated

Charging customers extra fees directly

Offering guarantees or extending banking services on their own accord

Continuing agency business after a criminal record involving fraud or dishonesty

Opening accounts, granting loans, or appraising loans (beyond permitted roles)

Accepting or cashing cheques

Transacting in foreign currency

Providing cash advances

Being run/managed by a bank’s employee or associate

Sub-contracting another entity (except within super-agent structures)

Revenue Models in Agency Banking

For agency banking to be sustainable, every player in the ecosystem; the bank or fintech, the agent, and even the regulator, needs to see value. The model is designed so that agents earn an income, customers pay affordable fees, and institutions maintain margins while scaling their reach. Revenue typically flows through a few key streams:

1. Transaction Fees from Customers

The most direct source of revenue comes from small fees charged on transactions such as cash withdrawals, deposits, bill payments, and transfers.

In Nigeria, for example, agents often charge ₦100–₦300 per withdrawal depending on the amount.

These fees are either fixed or tiered by transaction size.

The institution usually sets the pricing, and the revenue is shared with the agent.

It works because customers are willing to pay for convenience. Instead of traveling long distances or queuing in branches, they prefer paying a small fee to an agent within walking distance.

2. Commissions to Agents

Agents earn commissions as their primary incentive. This commission is usually a percentage of the transaction fee or a fixed payout per transaction.

The more transactions an agent processes, the more they earn.

High-volume agents (in markets or transport hubs) can earn substantial side income, making the role attractive.

It matters because a motivated agent is the backbone of the model. Fair commissions ensure agent loyalty and reduce churn.

3. Float Management & Balances

In agency banking, float refers to the pre-funded electronic balance that an agent maintains in their account with the bank or fintech. It’s essentially the digital counterpart of the cash they hold.

Here’s how it works in practice:

When a customer wants to deposit money, the agent collects the physical cash and deducts the same amount from their electronic float to credit the customer’s account.

When a customer wants to withdraw money, the agent gives them physical cash and the equivalent value is deducted from the customer’s account and added back to the agent’s float.

Because of this, agents must always manage two sides of liquidity:

Cash on hand – so they can handle withdrawals.

Electronic float – so they can process deposits.

If either side runs out, transactions fail. This is why super agents or aggregators often support sub-agents by helping them rebalance.

From the bank’s perspective, these pre-funded float balances (sitting in the institution’s system) create an additional revenue opportunity. They act like a pool of idle funds, which can earn interest or be strategically managed to optimise liquidity.

4. Value-Added Services (Cross-Sell)

Over time, agents evolve from handling basic cash-in/cash-out into distribution channels for higher-value services:

Savings products – onboarding customers into micro-savings accounts.

Loans – disbursement and repayment of microloans.

Utilities & subscriptions – electricity, water, cable TV, and airtime etc.

Each of these services creates new fee streams while increasing customer stickiness.

Considerations Before Going Into Agency Banking

Here’s what product managers and financial institutions must carefully evaluate before jumping in:

1. Product-Market Fit and Market Saturation

Before launching an agency banking solution, the key question is not "Can we build it?" but "Does the market truly need it?"

In Nigeria today, agency banking is highly saturated. Players like FirstMonie, Palm Pay, Quicktelller, Paga, OPay, Moniepoint, MTN MoMo etc already dominate with agent presence so dense that customers often have multiple options within walking distance.

This means access is no longer the problem, experience is. PMF here lies in solving what the current players haven't:

Are fees too high or inconsistent?

Do agents frequently run out of float?

Are customers lacking access to other value added services?

Are existing agents unsupported or poorly trained?

On the agent side, loyalty is hard-won. If your commissions, float support, or onboarding tools don’t clearly outperform, switching won’t happen.

To succeed, you need a clear answer to: Why would customers or agents choose us?

Differentiation could come through:

Better liquidity and float management

Transparent, fair pricing

Value-added services

Superior tools, training, or real-time agent support

Or you could play a different game entirely by providing the infrastructure or rails (POS devices, software, APIs) that empower other networks, rather than competing directly.

Point is, without PMF you risk burning capital on POS devices, partnerships, and recruiting, only to find there's no meaningful traction. With clear demand and positioning though, agency banking can become a strong, scalable growth driver.

2. To Build or to Partner

One of the most strategic decisions to be made is whether to build your own agent network or partner with existing super agents and solution providers

Building in-house means you recruit, onboard, train, and supervise agents directly. You own the full customer experience, control the commission structures, and set the standards for service quality. This approach gives you stronger brand presence and long-term control — but it comes at a high cost. Procuring POS devices and licences, building liquidity systems, hiring field officers, and running continuous support operations can be capital-intensive.

Partnering, on the other hand, allows you to tap into networks that already exist. Super agents, aggregators, and agent-banking-as-a-service providers have thousands of agents under them. By plugging into their systems, you scale faster and with lower upfront costs. However, you also give up some control over service quality, branding, and even pricing flexibility. And if you choose this path, thorough due diligence is non-negotiable — you must confirm your partners are licensed by the CBN, compliant with regulations, and capable of managing their networks responsibly.

The choice comes down to strategy. If agency banking is core to your growth and differentiation, investing in your own network might make sense despite the cost. But if it’s simply one distribution channel among many, partnering will get you to market faster. Either way, the trade-off is between speed and control and you must decide which matters more for your product and institution.

3. Regulatory Compliance

Agency banking in Nigeria is tightly regulated by the Central Bank of Nigeria (CBN). Financial institutions must apply for approval before launching agent networks, and agents themselves must comply with KYC, AML, and transaction limit requirements. Importantly, the principal institution remains fully liable for the actions of its agents, even if the agent acts outside the contract.

And compliance doesn’t stop at building your own network. If you choose to partner with existing super agents or aggregators, you still carry responsibility. Due diligence must be done thoroughly to confirm that your partners are properly licensed, compliant with CBN guidelines, and capable of managing their networks responsibly. Failing to check this can expose your institution to regulatory penalties, reputational risk, and even suspension of your agent banking operations.

4. Pricing and Commission Structures

Agents are not employees of the bank, they’re independent business owners. That means their motivation depends on whether the economics make sense for them. At the same time, customers in Nigeria are extremely price-sensitive, and banks/fintechs need to maintain margins. Getting the pricing and commission structure right is therefore one of the most delicate balancing acts in the model.

For agents, commissions are the lifeblood. If they don’t earn enough per transaction, they’ll either switch to serving competitors with better payouts or neglect agency services altogether. High-volume agents in busy locations expect stronger incentives, while those in smaller communities may need minimum guarantees or added support to stay active.

For customers, fees must feel fair. In Nigeria, most agents charge between ₦100–₦300 for withdrawals depending on the amount, with similar charges for transfers. Customers are willing to pay for convenience, but if fees climb too high, they’ll walk longer distances to cheaper agents or revert to cash-only transactions.

For institutions, margins must remain sustainable. Banks and MMOs typically split transaction fees with agents, but they must also cover infrastructure, support, and regulatory costs. Set commissions too high and profitability evaporates; set them too low and agents lose interest.

This is why many providers adopt tiered pricing models , adjusting commissions and fees by transaction size, geography, or service type. Some even introduce performance-based bonuses to reward high-performing agents.

5. Liquidity Management

A key factor that influences the reliability of any agent network is liquidity, i.e the agent’s ability to consistently maintain the right balance of cash and float to meet customer needs.

In practice, when either side is unavailable, transactions fail:

Cash but no float means deposits can’t be processed.

Float but no cash means withdrawals are impossible.

This challenge becomes more complex in Nigeria due to:

Geographic differences: Urban agents can rebalance more easily through nearby branches or super agents, while rural agents face longer travel times and limited access.

Seasonal surges: Events like salary periods, market days, or festive seasons often lead to sudden spikes in demand, which can quickly drain available liquidity.

As institutions explore agency banking, it’s important to reflect on whether the infrastructure and support systems in place can handle these fluctuations. This includes thinking about:

How agents will monitor their liquidity in real time ?

What safety nets exist to prevent prolonged outages?

Whether rebalancing support (via super agents or logistics partners) is accessible across all regions

From a product perspective, liquidity shortfalls translate directly to customer dissatisfaction. It’s not enough to have agents in place, they must be consistently able to serve. Any gaps here could erode trust, limit usage, and slow adoption, regardless of how wide the network becomes.

Agency banking reminds us that the best products are not just defined by design or functionality, but by how effectively they reach the people they’re meant for. A beautiful app won’t matter to someone who has no data, and a branch network won’t matter if it’s miles away.

By meeting customers where they already live and trade, agency banking turns everyday spaces into gateways of financial access. The model comes with real risks, but also transformative opportunities. For product managers, it’s proof that the most powerful solutions are those that deliver impact and business value at the same time.

See next week for another breakdown!

Another lovely read Seyi.

I’m glad I finally found the time to read your articles.

Good job.